Life policies are legal contracts and the terms of the contract describe the limitations of the insured events. Specific exclusions are often written into the contract to limit the liability of the insurer; common examples are claims relating to suicide, fraud, war, riot, and civil commotion.

Life-based contracts tend to fall into two major categories:

- Protection policies – designed to provide a benefit, typically a lump sum payment, in the event of specified event. A common form of a protection policy design is term insurance.

- Investment policies – where the main objective is to facilitate the growth of capital by regular or single premiums. Common forms (in the U.S.) are whole life, universal life, and variable life policies.

Life insurance was initially designed to protect the income of families, particularly young families in the wealth accumulation phase, in the event of the head of household's death. Today, life insurance is used for many reasons, including wealth preservation and estate tax planning. (For background reading, see The History Of Insurance In America.)

Life insurance provides you with the opportunity to protect yourself and your family from personal risk exposures like repayment of debts after death, providing for a surviving spouse and children, fulfilling other economic goals (such as putting your kids through college), leaving a charitable legacy, paying for funeral expenses, etc. Life insurance protection is also important if you are a business owner or a key person in someone else's business, where your death (or your partner's death) might wreak financial havoc.

Life insurance provides you with the opportunity to protect yourself and your family from personal risk exposures like repayment of debts after death, providing for a surviving spouse and children, fulfilling other economic goals (such as putting your kids through college), leaving a charitable legacy, paying for funeral expenses, etc. Life insurance protection is also important if you are a business owner or a key person in someone else's business, where your death (or your partner's death) might wreak financial havoc.

Who Needs It?Not everybody needs life insurance. If you are single and have no dependents, it may not be worth the expense. If, however, you have anyone who financially depends on you (even partially), life insurance may be appropriate for you. When considering life insurance, the questions to ask yourself are this:

- Do I need life insurance?

- How much do I need?

- How long will I need it?

- What type of policy makes sense for me? (this will be answered in our next section)

What Is Life Insurance?

New to buying life insurance? Learn how it works and what you need to understand to choose your coverage.

A life insurance policy is a contract with an insurance company. In exchange for premiums (payments), the insurance company provides a lump-sum payment, known as a death benefit, to beneficiaries in the event of the insured's death.

Typically, life insurance is chosen based on the needs and goals of the owner. Term life insurance generally provides protection for a set period of time, while permanent insurance, such as whole and universal life, provides lifetime coverage. It's important to note that death benefits from all types of life insurance are generally income tax-free.1

There are many varieties of life insurance. Some of the more common types are discussed below.

Term life insurance

Term life insurance is designed to provide financial protection for a specific period of time, such as 10 or 20 years. Typically, premiums are level and guaranteed for that time. After that period, policies may offer continued coverage, usually at a substantially higher premium rate. Term life insurance is generally a less costly option than permanent life insurance.

Needs it helps meet: Term life insurance proceeds are most often used to replace lost potential income during working years. This can provide a general safety net for your beneficiaries and can also help ensure the family's financial goals will still be met—goals like paying off a mortgage, keeping a business running, and paying for college.

It's important to note that, although term life can be used to replace lost potential income, life insurance benefits are paid at one time in a lump sum, not in regular payments like paychecks.

Universal life insurance

Universal life insurance is another type of permanent life insurance designed to provide lifetime coverage. Unlike whole life insurance, universal life insurance policies are flexible and may allow you to raise or lower your premium or coverage amounts throughout your lifetime. Like whole life insurance, universal life also has a tax-deferred savings component, which may build wealth over time. Additionally, due to its lifetime coverage, universal life typically has higher premiums than term.

Needs it helps meet: Universal life insurance is most often used as a flexible estate planning strategy to help preserve wealth to be transferred to beneficiaries. Another common use is long term income replacement, where the need extends beyond working years. Some universal life insurance product designs focus on providing both death benefit coverage and building cash value while others focus on providing guaranteed death benefit coverage.+

Whole life insurance

Whole life insurance is a type of permanent life insurance designed to provide lifetime coverage. Because of the lifetime coverage period, whole life usually has higher premiums than term life. Policy premiums are typically fixed, and, unlike term, whole life has a cash value, which functions as a savings component and may accumulate tax-deferred over time.

Fidelity does not currently offer whole life insurance.

Needs it helps meet: In addition to providing lifetime coverage, whole life is commonly used to accumulate tax-deferred savings. Whole life can also be used as an estate planning tool to help preserve the wealth you plan to transfer to your beneficiaries.

Comparing Types of Life Insurance

| Term Life Insurance | Universal Life Insurance | Whole Life Insurance | |

| Needs it helps meet | Income replacement in a lump sum | Wealth transfer, income protection and some designs focus on tax-deferred wealth accumulation | Wealth transfer preservation and tax-deferred wealth accumulation |

| Protection period | Designed for a specific period (usually a number of years) | Flexible; generally, for a lifetime | For a lifetime |

| Cost differences | Typically less expensive than permanent | Generally more expensive than term | Generally more expensive than term |

| Premiums | Typically fixed | Flexible | Typically fixed |

| Proceeds paid to beneficiaries | Yes, generally income tax-free | Yes, generally income tax-free | Yes, generally income tax-free |

| Investment options | No | No2 | No |

| May help build equity | No | Yes | Yes |

| Available through Fidelity | Yes, Fidelity Term Life Insurance3 | Yes, Universal Life Insurance, primarily focused on death benefit protection | Not currently offered |

Overview

Parties to contract

The person responsible to make payments for a policy is the policy owner, while the insured is the person whose death will trigger payment of the death benefit. The owner and insured may or may not be the same person. For example, if Joe buys a policy on his own life, he is both the owner and the insured. But if Jane, his wife, buys a policy on Joe's life, she is the owner and he is the insured. The policy owner is the guarantor and he will be the person to pay for the policy. The insured is a participant in the contract, but not necessarily a party to it.

The beneficiary receives policy proceeds upon the insured person's death. The owner designates the beneficiary, but the beneficiary is not a party to the policy. The owner can change the beneficiary unless the policy has an irrevocable beneficiary designation. If a policy has an irrevocable beneficiary, any beneficiary changes, policy assignments, or cash value borrowing would require the agreement of the original beneficiary.

In cases where the policy owner is not the insured (also referred to as the celui qui vit or CQV), insurance companies have sought to limit policy purchases to those with an insurable interest in the CQV. For life insurance policies, close family members and business partners will usually be found to have an insurable interest. The insurable interest requirement usually demonstrates that the purchaser will actually suffer some kind of loss if the CQV dies. Such a requirement prevents people from benefiting from the purchase of purely speculative policies on people they expect to die. With no insurable interest requirement, the risk that a purchaser would murder the CQV for insurance proceeds would be great. In at least one case, an insurance company which sold a policy to a purchaser with no insurable interest (who later murdered the CQV for the proceeds), was found liable in court for contributing to the wrongful death of the victim (Liberty National Life v. Weldon, 267 Ala.171 (1957)).

Contract terms

Special exclusions may apply, such as suicide clauses, whereby the policy becomes null and void if the insured commits suicide within a specified time (usually two years after the purchase date; some states provide a statutory one-year suicide clause). Any misrepresentations by the insured on the application may also be grounds for nullification. Most US states specify a maximum contestability period, often no more than two years. Only if the insured dies within this period will the insurer have a legal right to contest the claim on the basis of misrepresentation and request additional information before deciding whether to pay or deny the claim.

The face amount of the policy is the initial amount that the policy will pay at the death of the insured or when the policy matures, although the actual death benefit can provide for greater or lesser than the face amount. The policy matures when the insured dies or reaches a specified age (such as 100 years old).

Costs, insurability, and underwriting

The insurer (the life insurance company) calculates the policy prices or premiums to fund claims, administrative costs, and profit. The cost of insurance is determined using mortality tables calculated by actuaries. Actuaries are professionals who employ actuarial science, which is based on mathematics (primarily probability and statistics). Mortality tables are statistically based tables showing expected annual mortality rates. It is possible to derive life expectancy estimates from these mortality assumptions. Such estimates can be important in taxation regulation.

The three main variables in a mortality table are commonly age, gender, and use of tobacco, but more recently in the US, preferred class-specific tables have been introduced. The mortality tables provide a baseline for the cost of insurance, but in practice these mortality tables are used in conjunction with the health and family history of the individual applying for a policy to determine premiums and insurability. Mortality tables currently in use by life insurance companies in the United States are individually modified by each company using pooled industry experience studies as a starting point. In the 1980s and 1990s, the SOA 1975–80 Basic Select & Ultimate tables were the typical reference points, while the 2001 VBT and 2001 CSO tables were published more recently. The newer tables include separate mortality tables for smokers and non-smokers, and the CSO tables include separate tables for preferred classes.

Recent US mortality tables predict that roughly 0.35 in 1,000 non-smoking males aged 25 will die during the first year of coverage after underwriting.[13] Mortality approximately doubles for every extra ten years of age, so the mortality rate in the first year for underwritten non-smoking men is about 2.5 in 1,000 people at age 65. Compare this with the US population male mortality rates of 1.3 per 1,000 at age 25 and 19.3 at age 65 (without regard to health or smoking status).

The mortality of underwritten persons rises much more quickly than the general population. At the end of 10 years the mortality of that 25-year-old, non-smoking male is 0.66/1000/year. Consequently, in a group of one thousand 25-year-old males with a $100,000 policy, all of average health, a life insurance company would have to collect approximately $50 a year from each participant to cover the relatively few expected claims. (0.35 to 0.66 expected deaths in each year x $100,000 payout per death = $35 per policy). Other costs, such as administrative and sales expenses, also need to be considered when setting the premiums. A 10-year policy for a 25-year-old non-smoking male with preferred medical history may get offers as low as $90 per year for a $100,000 policy in the competitive US life insurance market.

Most of the revenue received by insurance companies consists of premiums paid by policy holders, with some additional money being made through the investment of some of the cash raised from premiums. Rates charged for life insurance increase with the insured's age because, statistically, people are more likely to die as they get older. The insurance company will investigate the health of an applicant for a policy to assess the likelihood of incurring a claim, in the same way that a bank would investigate an applicant for a loan to assess the likelihood of a default. Group Insurance policies are an exception to this. This investigation and resulting evaluation of the risk is termed underwriting.Health and lifestyle questions are asked, with certain responses or revelations possibly meriting further investigation. Life insurance companies in the United States support the Medical Information Bureau (MIB), which is a clearing house of information on persons who have applied for life insurance with participating companies in the last seven years. As part of the application, the insurer often requires the applicant's permission to obtain information from their physicians.

Underwriters will determine the purpose of insurance; the most common being to protect the owner's family or financial interests in the event of the insured's death. Other purposes include estate planning or, in the case of cash-value contracts, investment for retirement planning. Bank loans or buy-sell provisions of business agreements are another acceptable purpose.

In the USA, life insurance companies are never legally required to underwrite or to provide coverage to anyone, with the exception of Civil Rights Act compliance requirements. Insurance companies alone determine insurability, and some people, for their own health or lifestyle reasons, are deemed uninsurable. The policy can be declined or rated (increasing the premium amount to compensate for a greater probability of a claim), and the amount of the premium will be proportional to the face value of the policy.

Many companies separate applicants into four general categories. These categories are preferred best, preferred, standard, and tobacco. Preferred best is reserved only for the healthiest individuals in the general population. This may mean, that the proposed insured has no adverse medical history, is not under medication for any condition, and his family (immediate and extended) have no history of early-onset cancer, diabetes, or other conditions. Preferred means that the proposed insured is currently under medication for a medical condition and has a family history of particular illnesses. Most people are in the standard category. People in the tobacco category typically have to pay higher premiums due to the inherent health problems that smoking tobacco creates. Profession, travel history, and lifestyle factor into whether the proposed insured will be granted a policy, and which category the insured falls. For example, a person who would otherwise be classified as preferred best may be denied a policy if he or she travels to a high risk country. Underwriting practices can vary from insurer to insurer, encouraging competition.

Death proceeds

Upon the insured's death, the insurer requires acceptable proof of death before it pays the claim. The normal minimum proof required is a death certificate, and the insurer's claim form completed, signed, and typically notarized. If the insured's death is suspicious and the policy amount is large, the insurer may investigate the circumstances surrounding the death before deciding whether it has an obligation to pay the claim.

Payment from the policy may be as a lump sum or as an annuity, which is paid in regular installments for either a specified period or for the beneficiary's lifetime.

Insurance vs assurance

The specific uses of the terms "insurance" and "assurance" are sometimes confused. In general, in jurisdictions where both terms are used, "insurance" refers to providing coverage for an event that might happen (fire, theft, flood, etc.), while "assurance" is the provision of coverage for an event that is certain to happen. In the United States both forms of coverage are called "insurance" for reasons of simplicity in companies selling both products. By some definitions, "insurance" is any coverage that determines benefits based on actual losses whereas "assurance" is coverage with predetermined benefits irrespective of the losses incurred.

Types

Life insurance may be divided into two basic classes: temporary and permanent; or the following subclasses: term, universal, whole life, and endowment life insurance.

Term insurance

Main article: Term life insurance

Term assurance provides life insurance coverage for a specified term. The policy does not accumulate cash value. Term is generally considered "pure" insurance, where the premium buys protection in the event of death and nothing else.

Term insurance is significantly less expensive than an equivalent permanent policy. Term allows individuals with limited income to provide sufficient coverage for their family. Purchasers of term insurance should be aware that premiums for new insurance beyond the policy term will be higher because of advanced age. Future insurance needs beyond the policy term may be provided for by saving to provide for increased term premiums or by decreasing insurance needs (by paying off debts or saving to provide for survivor needs).

There are three key factors to be considered in term insurance:

- Face amount (protection or death benefit),

- Premium to be paid (cost to the insured), and

- Length of coverage (term).

Annual renewable term is a one-year policy, but the insurance company guarantees it will issue a policy of an equal or lesser amount regardless of the insurability of the applicant, and with a premium set for the applicant's age at that time.

Level premium term can be purchased in 5, 10, 15, 20, 25, 30 or 35 year terms. The premium and death benefit stays level during these terms.

Mortgage life insurance insures a loan secured by real property and usually features a level premium amount for a declining policy face value because what is insured is the principal and interest outstanding on a mortgage that is constantly being reduced by mortgage payments. The face amount of the policy is always the amount of the principal and interest outstanding that are paid should the applicant die before the final installment is paid.

Group life insurance

Group life insurance (also known as wholesale life insurance or institutional life insurance) is term insurance covering a group of people, usually employees of a company, members of a union or association, or members of a pension or superannuation fund. Individual proof of insurability is not normally a consideration in its underwriting. Rather, the underwriter considers the size, turnover, and financial strength of the group. Contract provisions will attempt to exclude the possibility of adverse selection. Group life insurance often allows members exiting the group to maintain their coverage by buying individual coverage.The underwriting is carried out for the whole group instead of individuals.

Permanent life insurance

Permanent life insurance is life insurance that covers the remaining lifetime of the insured. A permanent insurance policy accumulates a cash value up to its date of maturation. The owner can access the money in the cash value by withdrawing money, borrowing the cash value, or surrendering the policy and receiving the surrender value.

The three basic types of permanent insurance are whole life, universal life, and endowment.

Whole life

Whole life insurance provides lifetime coverage for a set premium.

Level premium whole life insurance (sometimes called ordinary whole life, though this term is also sometimes used more broadly) provides lifetime death benefit coverage for a level premium. Whole life premiums are much higher than term insurance premiums, but because term insurance premiums rise with increasing age of the insured, the cumulative value of all premiums paid under whole and term policies are roughly equal if policies are maintained to average life expectancy. Part of the insurance contract stipulates that the policyholder is entitled to a cash value reserve that is part of the policy and guaranteed by the company. This cash value can be accessed at any time throughpolicy loans that are received income tax-free and paid back according to mutually agreed-upon schedules. These policy loans are available until the insured's death. If any loans amounts are outstanding—i.e., not yet paid back—upon the insured's death, the insurer subtracts those amounts from the policy's face value/death benefit and pays the remainder to the policy's beneficiary.

Whole life insurance may prove a better value than term for someone with an insurance need of greater than ten to fifteen years due to favorable tax treatment of interest credited to cash values. However, for those unable to afford the premium necessary to provide adequate whole life coverage for their current insurance needs, it would be imprudent to purchase less coverage than is adequate as whole life insurance rather than purchase an adequate level of term to cover their current need.[19]

While some life insurance companies market whole life as a "death benefit with a savings account", the distinction is artificial, according to life insurance actuaries Albert E. Easton and Timothy F. Harris. The net amount at risk is the amount the insurer must pay to the beneficiary should the insured die before the policy has accumulated premiums equal to the death benefit. It is the difference between the policy's current cash value (i.e., total paid in by owner plus that amount's interest earnings) and its face value/death benefit. Although the actual cash value may be different from the death benefit, in practice the policy is identified by its original face value/death benefit.

The advantages of whole life insurance are its guaranteed death benefits; guaranteed cash values; fixed, predictable premiums; and mortality and expense charges that do not reduce the policy's cash value. The disadvantages of whole life are the inflexibility of its premiums and the fact that the internal rate of return of the policy may not be competitive with other savings and investment alternatives.

Death benefit amounts of whole life policies can also be increased through accumulation and/or reinvestment of policy dividends, though these dividends are not guaranteed and may be higher or lower than earnings at existing interest rates over time. According to internal documents from some life insurance companies, the internal rate of return and dividend payment realized by the policyholder is often a function of when the policyholder buys the policy and how long that policy remains in force. Dividends paid on a whole life policy can be utilized in many ways.

The life insurance manual defines policy dividends as refunds of premium over-payments. They are therefore not exactly like corporate stock dividends, which are payouts of net income from total revenues.

Modified whole life insurance features smaller premiums for a specified period of time, followed by higher premiums for the remainder of the policy.

Survivorship life insurance is whole life insurance insuring two lives, with proceeds payable after the second (later) death.

Limited-pay whole life

Another type of whole life insurance is limited-pay whole life insurance, whose premiums are paid over a specified period, commonly ten or twenty years, after which no additional premiums are due. Benefits are sometimes paid out at the age of 65; other ages can include 75, 85, and 100.

Other limited pay policies do not pay out at a set age, but become "paid up", leaving the policyholder with a guaranteed death benefit and no further premiums to pay.

Single-premium whole life insurance requires only one premium payment, paid at policy inception.

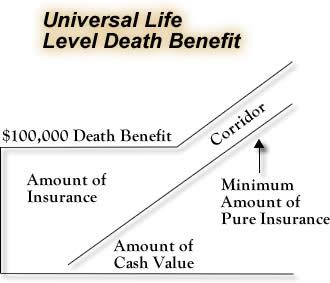

Universal life coverage

Universal life insurance (UL) is a relatively new insurance product, intended to combine permanent insurance coverage with greater flexibility in premium payments, along with the potential for greater growth of cash values. There are several types of universal life insurance policies, including interest- sensitive (also known as "traditional fixed universal life insurance"), variable universal life (VUL), guaranteed death benefit, and equity-indexed universal life insurance.

Universal life insurance policies have cash values. Paid-in premiums increase their cash values; administrative and other costs reduce their cash values.

Universal life insurance addresses the perceived disadvantages of whole life – namely that premiums and death benefits are fixed. With universal life, both the premiums and death benefit are flexible. With the exception of guaranteed-death-benefit universal life policies, universal life policies trade their greater flexibility off for fewer guarantees.

"Flexible death benefit" means the policy owner can choose to decrease the death benefit. The death benefit can also be increased by the policy owner, usually requiring new underwriting. Another feature of flexible death benefit is the ability to choose option A or option B death benefits and to change those options over the course of the life of the insured. Option A is often referred to as a "level death benefit"; death benefits remain level for the life of the insured, and premiums are lower than policies with Option B death benefits, which pay the policy's cash value—i.e., a face amount plus earnings/interest. If the cash value grows over time, the death benefits do too. If the cash value declines, the death benefit also declines. Option B policies normally feature higher premiums than option A policies.

Endowments

Endowments are policies which will pay a lump sum at either the death of the insured or after a set term, called the policy's maturity. Endowments require higher premiums than whole life and universal life policies because of the additional lump sum benefit at the maturity of the policy. Endowments are not technically permanent insurance because they do not cover the insured's lifetime, however they are commonly included in this class because of their high premiums.

The US Technical Corrections Act of 1988 tightened the rules on tax shelters such as modified endowments. These follow the same tax rules as annuities and IRAs.

Endowments mature and are paid out after a prespecified period (e.g. 15 years) or at a prespecified age (e.g., 65), whether the insured is alive or has already died.

Money back policy

A money back policy is a variant of the endowment plan. It gives periodic payments over the policy term. To that end, a portion of the sum assured is paid out at regular intervals. If the policy holder survives the term, he gets the balance sum assured. In case of death over the policy term, the beneficiary gets the full sum assured.

Accidental death

Accidental death insurance is a type of limited life insurance that is designed to cover the insured should they die as the result of an accident. "Accidents" run the gamut from abrasions to catastrophes but normally do not include deaths resulting from non-accident-related health problems or suicide. Because they only cover accidents, these policies are much less expensive than other life insurance policies.

Such insurance can also be accidental death and dismemberment insurance or AD&D. In an AD&D policy, benefits are available not only for accidental death but also for the loss of limbs or body functions such as sight and hearing.

Accidental death and AD&D policies very rarely pay a benefit, either because the cause of death is not covered by the policy or because death occurs well after the accident, by which time the premiums have gone unpaid. To know what coverage they have, insureds should always review their policies. Risky activities such as parachuting, flying, professional sports, or military service are often omitted from coverage.

Accidental death insurance can also supplement standard life insurance as a rider. If a rider is purchased, the policy generally pays double the face amount if the insured dies from an accident. This was once called double indemnity insurance. In some cases, triple indemnity coverage may be available.

Senior and pre-need products

Insurance companies have in recent years developed products for niche markets, most notably targeting seniors in an aging population. These are often low to moderate face value whole life insurance policies, allowing senior citizens to purchase affordable insurance later in life. This may also be marketed as final expense insurance and usually have death benefits between $2,000 and $40,000. One reason for their popularity is that they only require answers to simple "yes" or "no" questions, while most policies require a medical exam to qualify. As with other policy types, the range of premiums can vary widely and should be scrutinized prior to purchase, as should the reliability of the companies.

Health questions can vary substantially between exam and no-exam policies. It may be possible for individuals with certain conditions to qualify for one type of coverage and not another. Because seniors sometimes are not fully aware of the policy provisions it is important to make sure that policies last for a lifetime and that premiums do not increase every 5 years as is common in some circumstances.

Pre-need life insurance policies are limited premium payment, whole life policies that are usually purchased by older applicants, though they are available to everyone. This type of insurance is designed to cover specific funeral expenses that the applicant has designated in a contract with a funeral home. The policy's death benefit is initially based on the funeral cost at the time of prearrangement, and it then typically grows as interest is credited. In exchange for the policy owner's designation, the funeral home typically guarantees that the proceeds will cover the cost of the funeral, no matter when death occurs. Excess proceeds may go either to the insured's estate, a designated beneficiary, or the funeral home as set forth in the contract. Purchasers of these policies usually make a single premium payment at the time of prearrangement, but some companies also allow premiums to be paid over as much as ten years.

Related products

Riders are modifications to the insurance policy added at the same time the policy is issued. These riders change the basic policy to provide some feature desired by the policy owner. A common rider is accidental death (see above). Another common rider is a premium waiver, which waives future premiums if the insured becomes disabled.

Joint life insurance is either term or permanent life insurance that insures two or more persons, with proceeds payable on the death of either.

Unit Linked Insurance Plans

These are unique insurance plans which are basically a mutual fund and term insurance plan rolled into one. The investor doesn't participate in the profits of the plan per se, but gets returns based on the returns on the funds he or she had chosen.

The premium paid by the customer is deducted by initial charges by the insurance companies (basically the distribution and initial costs) and the remaining amount is invested in a fund (much like a mutual fund) by converting the amount into units based upon the NAV of the fund on that date.

Mortality charges, fund management charges, and a few other charges are deducted in regular intervals by way of cancellation of units from the invested funds.

A Unit Linked Insurance Plan (ULIP) offers high flexibility to the customer in form of higher liquidity and lower term.

The customer has the choice of choosing the funds of his choice from whatever his/her insurance provider has to offer. He can switch between the funds without the necessity to opt out of the insurance plan.

ULIPs got extremely popular in the heyday of the equity bull run in India, as the returns generated in equity linked funds were beating any kind of debt or fixed return instrument. However, with the stagnation of the economy and the equity market this product category slowed down.

With-profits policies

Some policies afford the policyholder a share of the profits of the insurance company – these are termed with-profits policies. Other policies provide no rights to a share of the profits of the company – these are non-profit policies.

With-profits policies are used as a form of collective investment scheme to achieve capital growth. Other policies offer a guaranteed return not dependent on the company's underlying investment performance; these are often referred to as without-profit policies, which may be construed as a misnomer.

No comments:

Post a Comment